Law firm profitability isn’t just a financial metric; it’s the lifeblood of your firm. Lacking a plan that actively strengthens the profitability of your practice will make it more difficult to compete with competitors, retain key talent, and, ultimately, grow your business.

These challenges make law firm profitability a complex puzzle to solve, especially considering how 15% of attorneys said getting paid is the most challenging part of running their firms, according to the AffiniPay 2024 Legal Industry Report.

Understanding how to identify and maximize the key elements of law firm profitability is essential to ensuring you have the resources to grow and succeed over the short and long term, and meet your law firm goals. A healthy profit margin puts you in a stronger position to better serve clients, attract the best talent, and capitalize on strategic opportunities.

While determining how to improve law firm profitability will vary, there are a number of considerations that can help you get started. In this post, we’ll define how to calculate law firm profitability, outline how law firms can measure their profitability, provide methods for boosting revenue and operational efficiency, and offer a sneak peek at the available technology to help you maximize your profitability efforts.

What Is Law Firm Profitability?

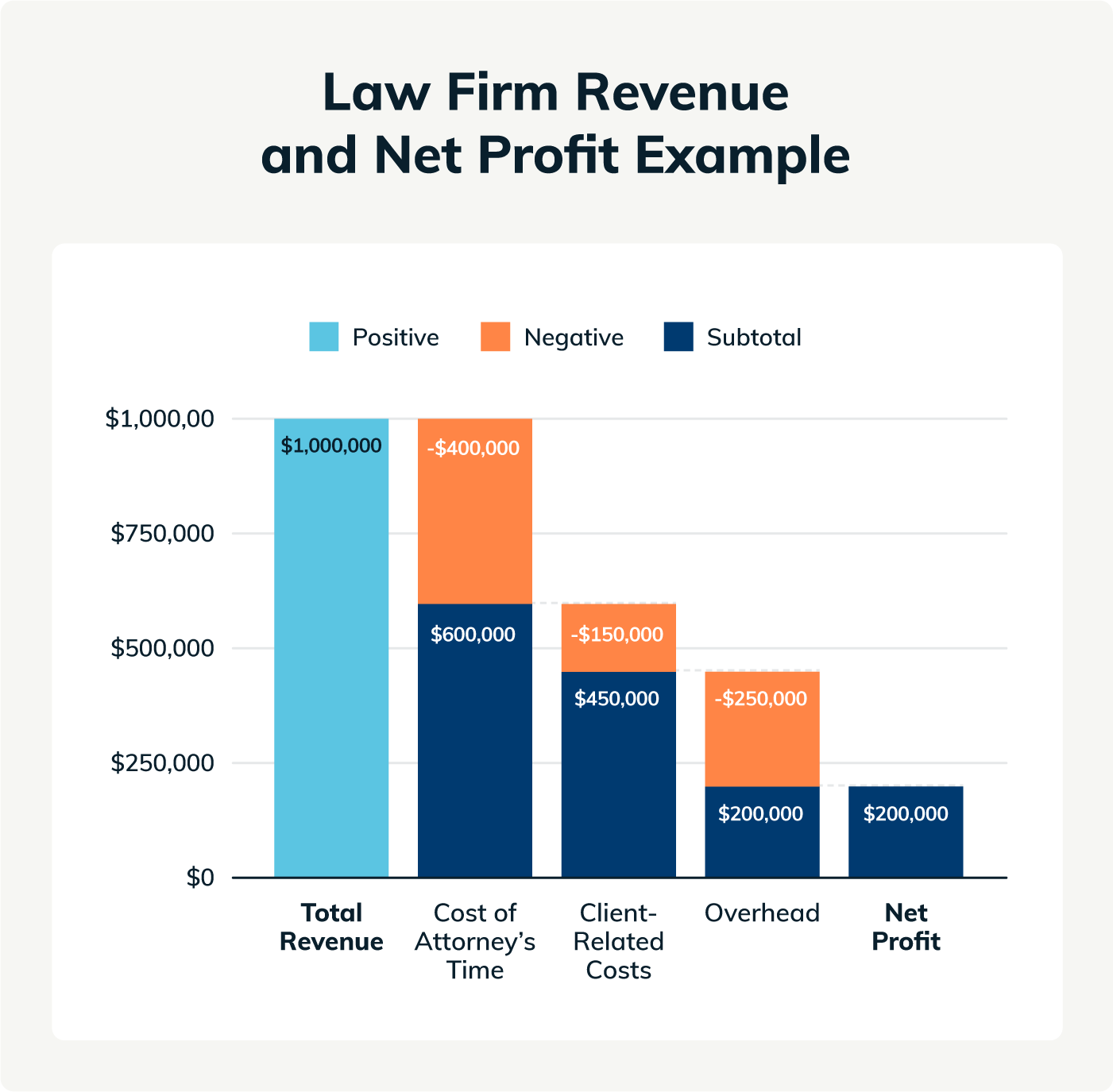

Law firm profitability is the revenue earned above the expenses incurred from running your practice. Your revenue is the money generated from billable hours, contingency fees, referral fees, and other income sources, while profit is the difference between the firm’s revenues and operating costs for running the practice.

With those factors in mind, this is how to calculate law firm profitability:

Revenue - (Cost of Attorney’s Time + Client Costs) = Gross Profit

Gross Profit - Overhead = Net Profit.

It’s common to assume that more revenue from clients and cases means higher profits, but that isn’t always true. Without finding ways to streamline your firm’s processes and cut costs, that extra work can add more operational costs, cutting your profits and putting your financial health at risk.

The key to maximizing law firm profitability and improving your firm's short- and long-term financial health is understanding your primary profit drivers and improving your operations in those areas. These drivers include:

Client acquisition costs: The less you spend to acquire each new client, the higher your margins will be as you build volume.

Efficiency: Streamlining administrative work through automation or outsourcing can reduce your practice's overhead operational costs.

Pricing strategy: A dynamic pricing strategy that provides more options to your clients can make it easier for them to pay you and reduce accounts receivable (A/R) headaches.

Workload balance: Finding ways to take non-billable hours off your plate and replacing that time with more billable work can provide a large boost to profitability.

Key Law Firm Profitability Metrics

When conducting a law firm profitability analysis, hundreds of possible key performance indicators (KPIs) can measure your practice's success. The ultimate goal of a law firm profitability analysis is to uncover actions you can implement quickly and easily to increase profits without sacrificing the high-quality service you provide to clients.

While there are hundreds of potential data points you can track, below are some of the most important law firm profitability metrics.

Billable and Non-Billable Hours

Law firm workloads are generally divided between billable and non-billable hours. Your least profitable time at the office is the time you spend completing non-billable work. While non-billable hours might be inevitable, there may be opportunities to delegate that work to administrative staff, hire a third party, or leverage legal automation tools to automate menial work and spend more time on generating high-value billable hours.

One easy implementation to consider is using law firm profitability time-tracking software. Our 2024 Legal Industry Trends Report found that lawyers who use the Smart Time Finder (a passive time tracking feature) captured an additional 579,667 hours, or about $22,425 in billable hours per lawyer.

Law Firm Leverage

Leverage is the ratio of associates to the number of equity partners at the law firm. The higher the ratio, the more associates and junior staff can handle lower-value work. This allows partners to focus on billable hours and provide more focused service to their clients. And since partners have a higher hourly rate, your overall law firm matter profitability may increase, even if you’ve hired more associate staff.

Reviewing your firm’s leverage ratio will help you determine if you have the capacity to add associates or support staff to your firm. Plus, you can further optimize time by giving these team members the right tools to automate repetitive tasks. For example, when you provide associates with the best law firm accounting software, they will have the tools to manage invoices, streamline billing and reporting, and reduce the time spent on administrative tasks, further enhancing your law firm matter profitability and return-on-investment (ROI).

Utilization Rate

A utilization rate measures an attorney’s billing efficiency and overall productivity. It’s measured by tracking the total hours worked against the number of billed hours. If a lawyer spends 50 hours a week in the office and spends 35 of those hours on billable tasks—their utilization rate is 70%. A low utilization rate indicates inefficiencies in your daily operations that cut into your profits.

Time tracking for law firm profitability gives you a direct view of your firm’s profitability issues by quantifying the time dedicated to billable vs. non-billable hours. Once you know how your time is divided, you can use that information to create clear goals for increasing billable work.

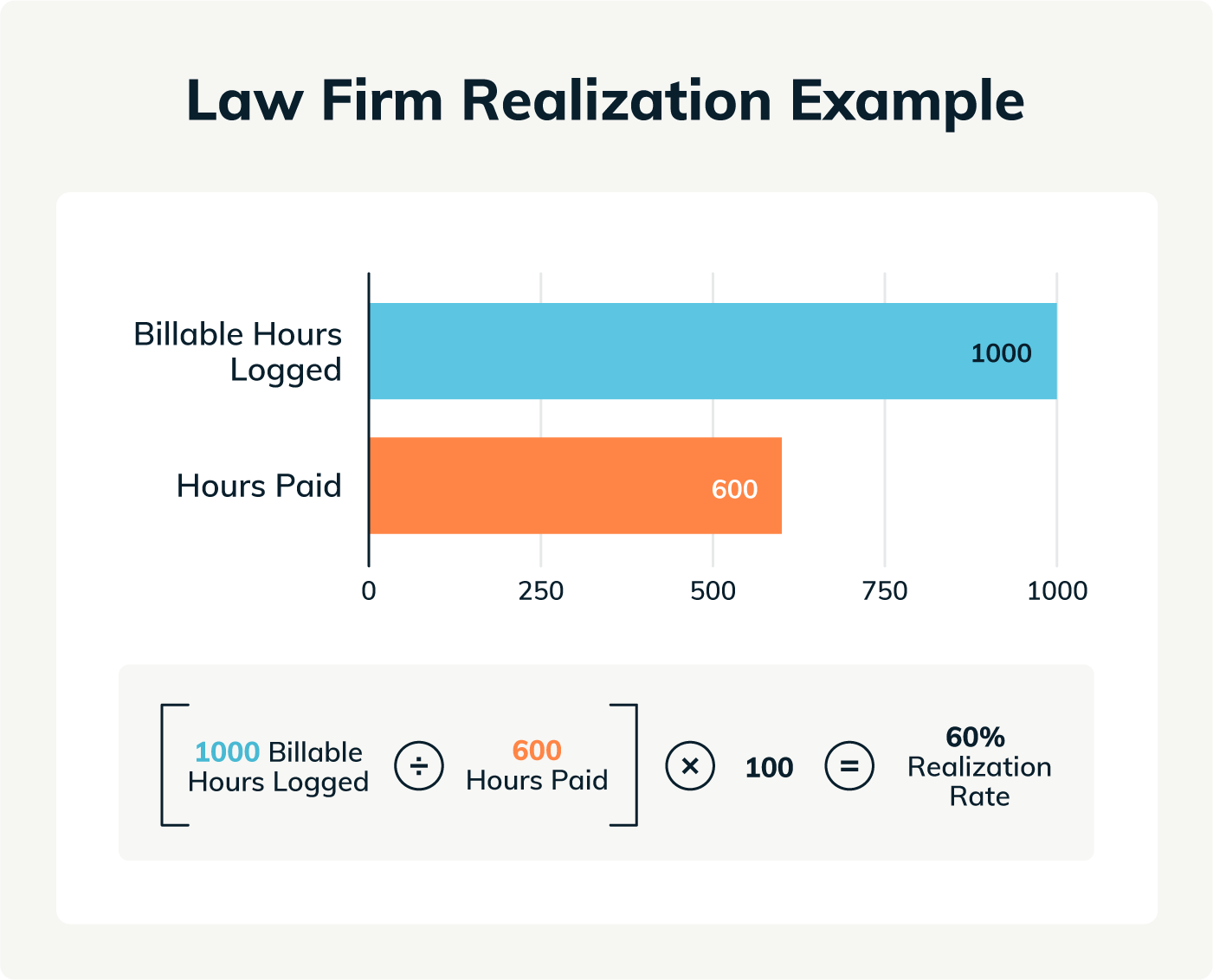

Realization Rate

A law firm realization rate is the number of billable hours you’ve accrued versus the amount you’ve successfully invoiced. For example, if an attorney bills all clients for 1,000 hours of billable work and collects 600 hours worth of fees, their realization rate is 60%. Like utilization rate, tracking realization rates is worthwhile because it can uncover patterns in cash flow indicative of law firm profitability issues.

There are several causes of low realization rates, including inefficient or inconvenient payment methods or an ineffective pricing strategy. It could also be due to more mundane (but equally important) reasons, such as errors during manual time tracking or other billing processes—like maintaining accurate records and generating reports.

Cash Flow

Law firm cash flow refers to the total amount of money coming in and out of your law firm over a specified period. Maintaining sustainable positive cash flow is important to keep your firm running smoothly, not only in the short term but also in investing in and growing your business over the long term.

Optimizing your law firm’s cash flow is imperative because payments are often not received immediately. Accurate cash flow tracking allows you to hone in on what’s most profitable and where your biggest inefficiencies lie.

Client Acquisition Cost

Client acquisition cost is the amount you pay to acquire new clients. These costs include website hosting fees, networking events, marketing, subscriptions, lead generation services, and more.

Analyzing your client acquisition costs provides a complete picture of the investments you’re making to obtain each client and, ultimately, the ROI of your acquisition expenditures.

Strategically streamlining acquisition costs ensures you’re effectively investing the firm’s resources to build a robust and profitable case pipeline.

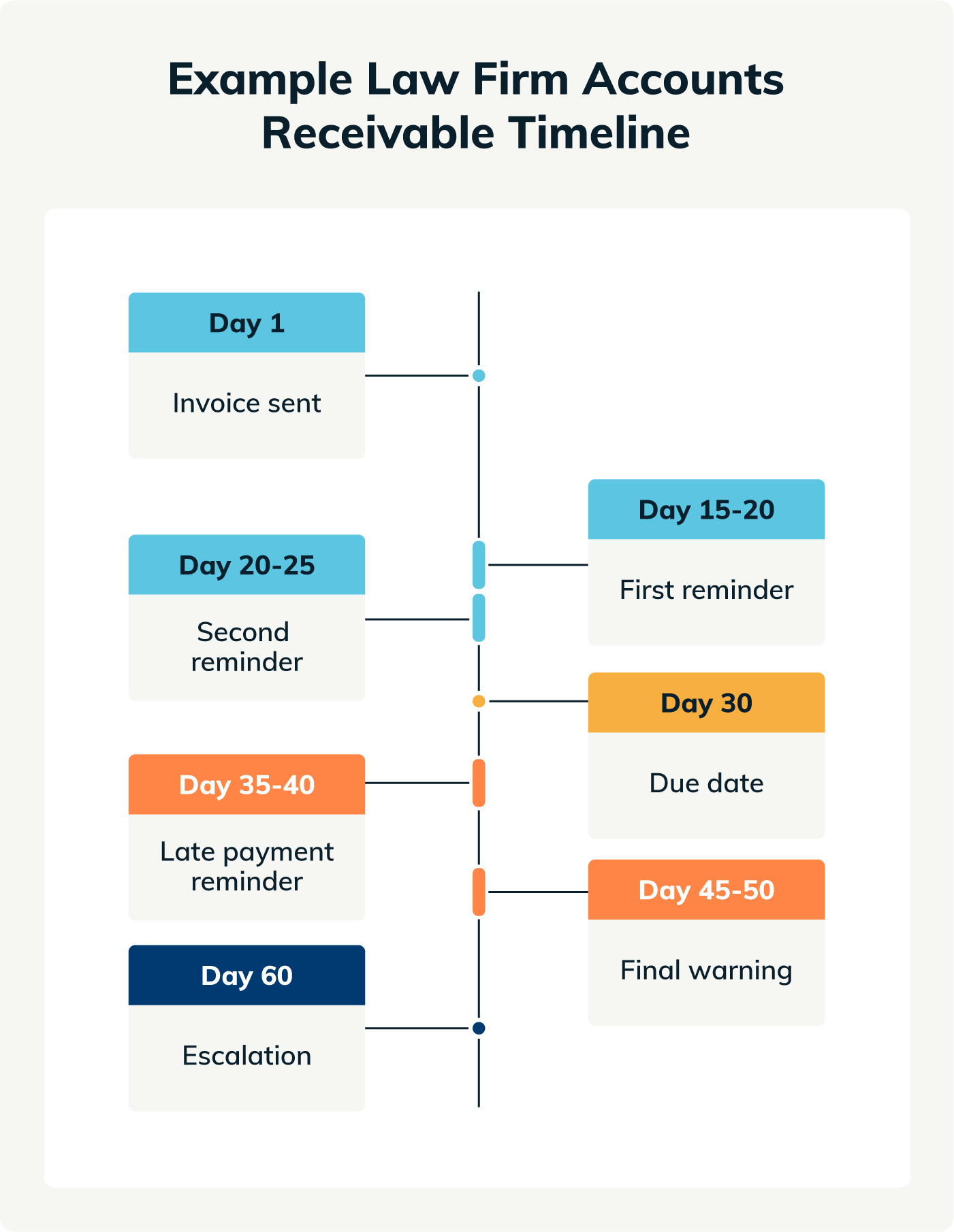

Outstanding A/R Balances

Retail businesses receive immediate payment for the services provided. Law firms have to invest in getting payment from their clients. Without an effective law firm A/R management strategy, the number of non-paying clients can increase along with the work that’s spent chasing down unpaid invoices. A/R values are only potential revenue until clients actually pay their bills. Identifying the causes behind your firm’s outstanding A/R balances is another key ingredient to improving cash flow and profitability.

A/R Turnover Rate

A/R turnover rate measures how long it takes for clients to pay you once you send an invoice. The underlying causes of high A/R turnover rates can include the following issues:

Failing to send invoices in a timely manner, which requires lawyers to spend time chasing down clients and requesting payments multiple times.

Implementing manual, rigid, or non-user-friendly billing processes, which creates friction that slows down the payment process.

Unhappy clients who try to dispute the bill and refuse payment, causing further delays in receiving compensation.

Streamlining this process through electronic invoicing, multiple payment options, and maintaining customer information can create a seamless payment experience for you and your clients. This can reduce the total A/R timeline and allow you to focus your energy on new clients rather than on clients whose cases you’ve already completed.

How to Improve Your Law Firm’s Profitability

Tracking your law firm’s financial data is a great starting point for increasing profitability. It will help you hone in on problem areas and make better decisions. As you get a clearer picture of your firm’s financial health, there are a few aspects of your firm’s operations you can consider when finding opportunities to drive profits:

1. Set and Track High-Quality Goals

Implementing a law firm profitability tool can help you measure important KPIs when working to increase profits. Some KPIs that you may want to measure include:

A/R turnover rates and balances

Billable and non-billable hours

Cash flow

Client acquisition costs

Leverage

Realization and utilization rates

Once you’ve finalized the KPIs you want to measure, you can establish realistic benchmarks for your law firm. The more straightforward your reporting system is, the easier it will be to measure your success and failure rate in improving the profitability of your practice.

2. Re-evaluate Pricing

You don’t use a one-size-fits-all approach when working with your clients. Instead, you take the time to learn about their situation and develop a tailored plan that puts them in a favorable position to succeed.

When considering your pricing, a flexible model tailored to each client can be more beneficial for both parties. There are several types of flexible fee arrangements that may be appropriate for your firm:

Hourly rate

Flat-rate fee

Contingency pricing

Retainer

Versatile pricing structures can be a differentiator that sets you apart from your competitors. Plus, figuring out the pricing that works best for each client can reduce some of the headaches associated with A/R management.

3. Review Client Acquisition and Referral Methods

Finding ways to reduce expenses related to client acquisition is an immediate boost to profitability. To understand the ROI of each client acquisition method, keep track of how much you’ve spent on a method, how much time you dedicate on average to that method, and how many leads and clients that method delivers to your firm. Regularly analyzing these metrics helps you make data-driven decisions around budget adjustments and prioritization.

For example, let’s say you invest in both online advertising and print advertising in local publications. After keeping track of both approaches for a few months, you may determine that online advertising delivers more total leads per dollar spent. Based on this, you can choose to reallocate more of the budget to online advertising to maximize your investment.

You can also look for more affordable client acquisition methods to replace more time-consuming or expensive strategies. One low-cost method of client acquisition is establishing a referral program where satisfied clients tell friends and family about your practice. By maintaining positive relations with your clients throughout the legal process, you can empower satisfied clients to become vocal advocates who enthusiastically endorse you to their friends and family.

4. Delegate or Outsource Tasks

When your firm was smaller, you may have easily handled the non-billable tasks yourself. As your firm continues to grow, handling these non-billable tasks drains your profitability. Because partners at a law firm command the highest billable rates, their schedules should compromise as much billable work as possible to maximize profitability.

More administrative and less valuable tasks should be delegated to associates, paralegals, or other staff members so that you can focus on increasing your billable hours. Alternatively, if there is no one on staff to handle this work, partnering with a third party to outsource this work is another option. Tasks that you should consider delegating or outsourcing include:

Accounting and payroll

Administrative work

Client intake

HR

IT and technology management

5. Automate with Legal Software

Lawyers can automate administrative tasks using software such as:

Billing and collections

Client intake

Customer relationship management (CRM)

Document management

Practice management

Time tracking

While there is an increasing opportunity to automate, attorneys should still be diligent in determining what tasks can be offloaded and what tasks they should keep. For example, tasks that are more legally complex or projects for high-value clients may need to stay with a lawyer.

6. Bill and Collect Efficiently

Specialized legal billing software solutions provide an easy way to modernize and streamline your collection and payment processes. During intake, be sure to discuss your billing policy with your clients by discussing the billing and payment options you have available. This improves the client experience and results in faster payments without spending more hours on collections.

7. Reduce Expenses

To effectively reduce expenses, you must first start tracking all of your financial data to give you a clear picture of your spending. This will help ensure you are cutting unnecessary or bloated expenses in your budget without sacrificing quality representation and customer service. Some ideas for reducing recurring expenses include:

Cancelling rarely or never-used online subscription services

Digitizing documentation

Reducing office space or considering a virtual office

Implementing automation software

8. Offer Alternative Ways to Pay

When it’s easier for clients to pay their legal bills, your firm gets paid faster. Legal billing solutions make it easy to implement alternative payment methods for law firms. By offering credit cards and other digital payment options, law firms can consistently get paid faster and more reliably.

Flexibility entails more than just payment methods—it can also apply to payment plans or Pay Later billing options. Our 2024 Legal Industry Trends Report found:

48% of law firms collected more money over the course of a case by using payment plans.

47% of law firms that offer a Pay Later (legal fee funding) option could accept more cases.

These offerings reduce the pressure that comes with requiring payment in one lump sum.

9. Routinely Review Financial Data

Improving your law firm’s profitability is not a one-time activity. Conducting ongoing law firm profitability reporting is an essential element to adjusting your practice over time.

After setting high-quality goals, your firm can track them using a law firm profitability tool. How well your firm accomplishes your goals will impact future years’ budgeting, forecasting, and financial reporting.

At regular periods, you and other important stakeholders should review key legal analytics data to help gauge how well you’re performing toward your goals. Law firm profitability reporting will vary depending on the KPIs you opt to monitor for your practice.

For example, if you are focused on improving the efficiency of your time, you’ll likely want to review metrics like billable and non-billable hours. If you are lagging behind your billable hours goal, you may want to consider:

Hiring more staff

Outsourcing non-core responsibilities

Automating some of your administrative tasks

Improve Your Law Firm’s Profitability With LawPay

Improving your law firm’s profitability requires more than just increasing your revenue—it demands a comprehensive plan that analyzes all aspects of your firm’s business and structure. By finding ways to increase efficiencies in your law firm’s operations, you can free up time to focus on growing your billable hours, improving profitability, and investing in your practice.

Successful firms can increase their profitability by knowing exactly how their money is coming in, where they spend it, and where inefficiencies lie. LawPay Smart Spend allows you to simplify expense reporting for your staff, reduce the risk of unnecessary spending, and manage all of your finances in a single platform. Sign up for early access today and start managing your firm’s finances with ease.

To find out how LawPay is helping thousands of practices take control of their finances, schedule a demo today.

Schedule a demo to see what LawPay can offer your firm.

Get a demo

About the author

Esther Park is a Content Writer and Senior SEO Manager at 8am. Her expertise lies in writing about emerging legal technologies and financial wellness strategies for law firms, among other topics.