Legal accounting is notoriously complex, and many attorneys receive little training on how to manage IOLTA accounts properly. Ideally, law firms follow strict rules for handling client funds and use cases. While requirements vary slightly between state bar associations, all lawyers are required to deposit unearned client funds into a separate trust account—commonly called an IOLTA or Interest on Lawyer Trust Account. Mismanaging or commingling funds can result in serious consequences, including reprimand or even disbarment.

Even honest mistakes can damage your reputation and erode client trust. By understanding how IOLTAs work, following best practices, and using the right tools, your firm can stay compliant and focus more on serving clients.

What is an IOLTA Account?

An IOLTA is a specialized trust account that firms use to hold client funds they have not yet earned, such as retainers, settlement proceeds, or court-related fees. Firms keep these funds entirely separate from a lawyer’s operating or personal accounts to comply with ethical and legal standards. Attorneys are also prohibited from profiting off any interest generated by these accounts.

IOLTA programs were introduced in the 1980s to help law firms pool smaller or short-term client funds into a single interest-bearing account. Since the interest earned from individual accounts would often be negligible, this pooled approach allows those funds to generate meaningful interest.

Firms then direct that interest to state bar associations to support access-to-justice initiatives, including legal aid for low-income individuals and public service programs.

Difference Between IOLTA vs IOLA

IOLTA and IOLA (Interest on Lawyer Account) essentially serve the same purpose—to manage client funds temporarily held by lawyers. The key difference is in their geographical applicability. IOLTA is the broader term used across most states, whereas New York uses the term IOLA.

Difference Between IOLTA vs Attorney Trust Account

Attorney trust accounts hold substantial or long-term client funds, with the interest benefiting the individual client. The primary distinction between an IOLTA and an attorney trust account is who benefits from the interest—public services for IOLTA versus the client for standard attorney trust accounts.

Difference Between IOLTA vs Escrow Account

Escrow accounts, used in various transactions, hold funds neutrally until conditions are met, with interest distribution specified by the escrow agreement. Similar to the attorney trust account mentioned above, a major difference between an escrow account and an IOLTA is in their interest beneficiaries—public services benefit from IOLTAs, whereas designated parties benefit in escrow accounts.

When is an IOLTA Account Used?

Any time a law firm accepts payments for retainers from clients or handles money on a client’s behalf, it is put into an IOLTA. Legal fees that are not part of a retainer can generally go directly into an operating account since the payment is not for future work.

While any unearned client money is required to be deposited into a trust, it may or may not be mandatory to use an IOLTA, depending on the rules in your state. It’s best to check in directly with your state bar association or a legal account expert to confirm whether or not using them is required. That said, given that an IOLTA raises money for a number of worthy causes, it’s almost always beneficial to use them.

How Do IOLTA Accounts Work?

To understand how IOLTA accounts work in practice, let’s walk through a simple example:

Client payment: Client A signs a retainer agreement and pays a $7,000 retainer to secure your legal services. That money is placed into your IOLTA account because it hasn’t been earned yet—it’s considered unearned and must remain separate from your business funds.

Work begins: A week later, you work 4 hours on Client A’s case at $120/hour, totaling $480 in legal fees.

Client approval: Even after the work is complete, you can’t withdraw the $480 until Client A reviews and approves the invoice. Only then is the amount considered earned.

Fund transfer: Once approved, you transfer the $480 from the IOLTA account to your firm’s operating account. The remaining $6,520 stays in trust until additional work is completed and billed.

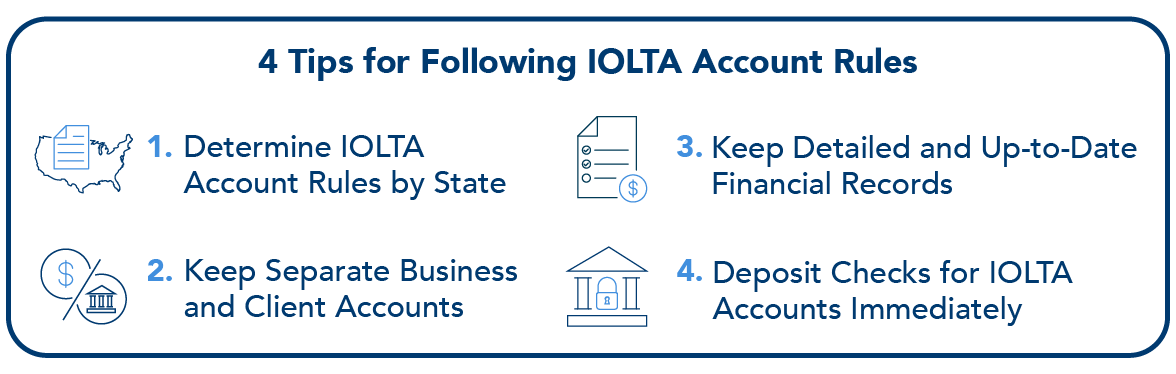

4 Tips for Following IOLTA Account Rules

While this all may seem simple enough on paper, properly handling an IOLTA can be incredibly complex and time consuming in practice. There are strict rules for how the money in them must be used and recorded. Even a large law firm with a dedicated accounting team has to take deliberate steps to maintain IOLTA compliance.

Smaller law firms or independent attorneys have to be infinitely more careful since small mistakes can have dire consequences. It’s also worth noting that a lawyer is always on the hook for misusing funds from an IOLTA, even if the mistake is made by a bookkeeper or paralegal.

Here are several law firm accounting best practices to keep in mind so you always handle an IOLTA trust account properly:

1. Determine IOLTA Account Rules by State

IOLTA account regulations differ across states, each having its own unique rules on how legal professionals manage client funds. These variations encompass aspects such as reporting requirements, the handling of nominal or short-term funds, and the specific criteria for when funds should be deposited into IOLTA accounts versus individual client trust accounts. For instance, some states mandate periodic reporting to state bar associations, while others require specific procedures for client notification.

Despite these differences, common threads run through all IOLTA programs. These commonalities include the necessity for law firms to clearly label accounts as trust or client accounts and maintain a strict separation between client funds and personal or business funds. Detailed record-keeping is also universally mandated to ensure transparency and accountability. Additionally, the interest generated from these pooled accounts is consistently directed toward funding legal aid and public interest programs, promoting access to justice across different jurisdictions.

For additional information on IOLTA account regulations in your state or jurisdiction, refer to the American Bar Association’s guidelines here.

2. Keep Separate Business and Client Accounts

Commingling funds from a law firm’s operating account and a client trust fund are strictly prohibited by state ethics rules. This is why it is essential for law firms to maintain separate operating and trust accounts. Sometimes, the distinction can be confusing since completed work is paid out from funds that are held in an IOLTA. So what exactly do we mean by “commingling funds”?

“Borrowing” or withdrawing from client IOLTA accounts: An IOLTA or any other kind of client trust account is not a savings account. Sometimes, law firms find themselves faced with impending bills and other big expenses before completing billable work, and it can be tempting to draw from retainer money to stay afloat. But this kind of “borrowing” can have serious consequences, even if you have every intention of quickly paying it back. Until work is properly completed and billed, retainer money is off-limits. Additionally, even if client funds are billed and earned, the money must be transferred to the business account first before being withdrawn. Should an IOLTA account issue a debit card, be very careful it is not used to withdraw money directly from the account in those circumstances.

Depositing client funds into a business account: Sometimes attorneys are unsure of what funds are meant to go into a trust and which aren’t. For example, if a client without a retainer pays attorney fees, that money may be able to go directly into an operating account. But what if a client pays fees for an attorney’s services and court filing fees together? Even if the filing fees are minuscule, the entire amount would have to be deposited into an IOLTA trust account first.

Charging payment fees to an IOLTA: Money from an IOLTA cannot be used to pay for third-party processing fees or charges for electronic payments. This also includes any fees to maintain the trust account itself. Instead, these charges must be taken out of the operating account. These mistakes can be surprisingly easy to miss without specialized tools and software.

Keeping business and trust accounts separate is simply the only way to reduce your IOLTA compliance risk. However, as many state bar associations have specific requirements for establishing and administering IOLTAs and other legal trust accounts, it’s always best to consult an expert.

3. Keep Detailed and Up-to-Date Financial Records

One of the most common ways that law firms run into trouble is by not keeping detailed financial records of every single client’s trust account transactions. That means maintaining separate ledgers for each client and keeping track of all payments, no matter how insignificant they may seem. Additionally, IOLTA transactions should be recorded the moment they happen to avoid anything from slipping through the cracks.

To further prevent any errors, IOLTA debits and credits should be recorded using a double-entry accounting system. While manually keeping track of this can be a logistical nightmare, legal billing software like LawPay can significantly streamline and simplify the process.

4. Deposit Checks for IOLTA Accounts Immediately

Related to the point above, attorneys must always have an accurate and up-to-date record of where clients’ funds are at any given time. While an increasing number of law firms accept payment electronically these days, some clients still prefer to pay by check. In those cases, don’t wait to deposit it. Ultimately, a client’s retainer check is not yet your money, and that money must be immediately accessible to them.

Ensure IOLTA Account Compliance with LawPay

IOLTA accounts are a useful way to keep client funds separate from a law firm’s operating expenses while benefiting the community. However, as previously mentioned, trying to administer them manually using spreadsheets or non-specialized accounting software can open you up to risk. This gets even more complex as more law firms continue to modernize by offering digital payments for their clients since even small payment processing fees have to be handled correctly to stay IOLTA compliant.

Luckily, legal billing software like LawPay takes the complexity out of record keeping and IOLTA compliance. LawPay’s industry-leading payment solution was created in cooperation with bar associations and ethics committees to ensure all types of payments are processed correctly and in compliance with the IOLTA guidelines in your state. A variety of powerful, best-in-class features help you easily manage your client trust and streamline your payment processes.

Automatic Separation of Earned and Unearned Funds

LawPay connects to both your trust and operating accounts, ensuring your earned and unearned funds remain separate. Strict payment processing rules take the guesswork out of account management, as funds are automatically moved into the correct accounts.

Streamlined Record Keeping

Unintentional gaps in your records can snowball into big problems later on. LawPay drastically simplifies record keeping by making relevant and detailed notes of every transaction. Multiple trust and IOLTA accounts can be linked into LawPay’s system, giving you a comprehensive and consistent way to track client funds and operating costs in real-time.

Compliant Payment Processing Practices

As we’ve discussed, payment processing fees, including those by third parties, cannot be taken from a trust account. LawPay strictly prohibits debits from your trust account for any reason, and all processing fees are automatically tracked and debited from your operating account at the end of the month.

Improve Compliance with Existing Software

With robust integrations, including the best law firm accounting software and legal operations, LawPay adds an additional layer of security to your existing processes.

Schedule a demo to see what LawPay can offer your firm.

Get a demo

Ready to Learn More?

When it comes to effectively managing an IOLTA account, your law firm can’t afford to take risks. Schedule a LawPay demo to find out how LawPay can help you manage your trust accounts, minimize compliance risk, and give you more time to focus on your clients.

About the author

The LawPay Team