Key takeaways

Determining the best law firm accounting software for your practice is important. Learn the key features for law firms and how to choose the right software.

You're a lawyer, not an accountant. We know you'd like to spend your limited time in other ways. But setting up your finances properly won't just make it easier to file your taxes each year—it'll save you time, money, stress, and potentially legal trouble. Using a legal accounting solution can make an especially big difference.

Our 2024 Legal Industry Report found that 28% of legal professionals use legal accounting software rather than consumer accounting software like Quickbooks. Of those respondents, 46% say it saves them 1-5 hours each week.

When implementing a law firm accounting strategy, there is plenty to consider. From creating a budget to choosing the right bank and hiring the correct advisors can feel overwhelming.

The following guide explains the fundamentals of law firm accounting and bookkeeping. We'll also show you how you can make the whole process easier.

What Is the Difference Between Legal Accounting and Bookkeeping?

Legal accounting and bookkeeping are vastly different, though many people use the terms interchangeably. Legal bookkeepers and legal accountants work with your firm's financials with the shared goal of helping your firm financially grow and succeed. But what they do with that data (and when) varies. Regardless, each serves a purpose at your firm.

Law Firm Bookkeeping

Law firm bookkeeping records the financial transactions and balances of your firm’s financial accounts. Legal bookkeeping takes place before any accounting can occur and is an essential administrative task for any law firm. Reliable bookkeeping for attorneys also provides accurate financial data for legal accountants to work with.

Legal Accounting

Legal accounting consists of more complex accounting tasks. This includes preparing tax returns and reconciling bank statements with general and client ledgers. Legal accounting also goes one step further by taking a high-level look at a law firm’s financial health by forecasting, creating budgets, and identifying areas for growth.

Choose the Right Law Firm Accounting Software

It's no secret that accounting is tedious. The bad news? You can't use Excel spreadsheets to maintain all of your financial books and records for an entire year. When used for that much data, Excel becomes clunky and lacks features you could use to improve your reporting. The good news? There are plenty of great law firm accounting software solutions available that can help get you started.

Keeping accurate records of your law firm's accounts is a challenging yet vital part of running a legal practice. Legal accounting software simplifies your firm's accounting and bookkeeping workflows—making it easier to stay compliant with ethics rules, protect sensitive client information, and effectively monitor your day-to-day cash flow.

The advantages of legal accounting software multiply with today's cloud-based solutions.

While on-premise accounting software ties you to a physical location and requires high maintenance costs and time-consuming updates, cloud-based accounting software is accessible anywhere.

Cloud-based accounting software for law firms also automatically gets updated and backed up—offering unparalleled, real-time insights into your firm's financial data.

Before purchasing software, ensure it fits your needs. A solid law firm accounting solution should include features such as:

Billing and invoicing

Bookkeeping

Reporting and analytics

Expense tracking

Payroll

Tax prep

MyCase Accounting is a comprehensive legal accounting solution that houses case and financial data in one IOLTA-compliant platform.

By centralizing data and automating three-way trust reconciliation, you can clearly understand your firm’s financial health. MyCase streamlines the legal accounting process to save you time and make it easy for your firm to manage accounting internally rather than trying to do it yourself manually or completely outsourcing it to a third party.

To streamline tasks even more, consider using LawPay’s payment integration with MyCase to easily combine your payment platform with MyCase’s end-to-end suite of features for law firms. By doing so, your law firm can easily keep track of accounts receivable and the status of your clients’ accounts.

You can also integrate LawPay with generic accounting tools to easily track clients, invoices, and more. For example, if you use LawPay to collect payments and invoice clients, you can easily sync all your transactions into QuickBooks for easy reporting and reconciliation.

Hire Outside Help As Needed

Managing your books via accounting software may get you started as a solo attorney. But, if you want to spend your time focused on practicing law rather than deep in the weeds of your law firm’s accounting and financial management, you may want to consider hiring help. There are several options available. One (or more) of these professionals can greatly assist with your law firm's accounting.

Bookkeeper

A bookkeeper records your firm’s daily transactions. In addition, they may help you create and send invoices, process your accounts payable, manage payroll, and run routine financial reports.

In short: If you'd like to save time and keep your finances a little more organized, a bookkeeper can help keep your records updated and your business expenses categorized.

Controller

While a bookkeeper keeps the day-to-day data accurate and updated, a controller can help you set up and oversee your financial system and accounting infrastructure. Controllers often oversee the bookkeeper's work, reconcile the accounts, and make more significant ledger adjustments.

In short: If you'd like a deeper understanding of financial trends within your business, a controller can use your financial data to understand what it tells you about your business.

Accountant or CPA

Accountants analyze, interpret, and summarize financial data. Legal accountants use financial data that a bookkeeper records as a way to strategically help your firm. They perform tasks for law firms, such as preparing financial statements, providing financial forecasting, and capturing expenses.

In short: CPAs use their expertise and an analysis of your finances to help you leverage your business through loans and investments and ultimately build a financial management plan for your law firm.

Set a Budget for Your Law Firm

The basis of good legal accounting always starts with a well-thought-out budget. A law firm budget helps you set expectations regarding cash flow and expenses for the year—reducing the likelihood of missing a payment or bouncing a check. Your law firm can also set revenue benchmarks, which will help you determine if you are meeting your goals or need to adjust your business plan.

Below are steps to take to set a budget:

Brainstorm your firm's expenses: For each line item you consider adding to your budget, ask yourself three big questions: Will this save me time to put towards more billable work? Will this help me find more business? Do the benefits outweigh the cost?

Identify current resources: You'll also want to outline what assets you have on hand, such as starting capital and existing equipment. Refer to your law firm’s chart of accounts and make updates as needed.

Make a savings plan: Set aside some money, either as a recurring expense or a percentage of your revenue, for any potential surprises you encounter.

Project your revenue: Once you've itemized all the expenses, resources, and savings to set aside, the next step is to project your expected revenues. Also incorporate your personal and business goals into the process.

Set rates: Be sure to set your rates carefully, factoring in the objectives above and the average rates for your location and practice area.

Document and track your budget: This will give you a sense of whether you need to adjust your projections or document any expenses you didn't account for. You should also set aside time to formally review your budget each year.

To help with ongoing financial management, learn more about LawPay’s Legal Spend Management Solution. Our tool provides a comprehensive view and real-time insights into your law firm’s finances.

Set Up Your Firm’s Bank Accounts

As every business is different, your choice of the "right bank" depends on the nature of your practice, as well as how you prefer to handle your banking transactions.

When comparing options, consider the following questions:

Does the bank support your Point of Sale (POS) system?

What does the bank offer in terms of security and fraud protection?

Does the bank's online banking option let you designate separate users (for business partners, if necessary)?

What kind of fees are they going to charge you?

To open any business bank account, your practice needs to be registered with the state in which you are operating, have a registered business name, and have an Employer Identification Number (EIN). Before meeting with a bank representative, call ahead and ask what paperwork you need to bring to your initial appointment.

What Types of Bank Accounts Does Your Firm Need?

Once you've chosen a bank to work with, there are four types of accounts you'll want to open:

Business checking account: You will manage most of your business expenses and revenue from your checking account.

Business savings account: Set aside money you'll need later in a savings account. Even though interest rates on business accounts are traditionally low, having a cash surplus in a business savings account can improve your likelihood of being approved for a loan.

IOLTA account: In addition to business checking and savings accounts, most law firms are required to hold client funds in a separate legal trust account—often called an "IOLTA”.

Business credit card: Although not required, opening a business credit card can help your law firm separate business expenses from personal expenses. LawPay’s upcoming Legal Spend Management Solution is another option to consider if you’d like an approached tailored for law firms.

If you have employees, you will need to set up payroll. Ask your bank about payroll services and if they partner with payroll services to help you get started.

What to Know About IOLTA Accounts

IOLTA accounts are tricky because they have very specific rules around what you can and can't do with them, and the penalties for breaking these rules can be severe—including disbarment.

Every state has an IOLTA program, and it's likely that the bank where you opened your regular business checking account also offers IOLTA accounts. But rules vary by state, so consult your State Bar Association and a professional accountant before finalizing your accounting setup.

For peace of mind, we recommend seeking a payment and billing provider that adheres to IOLTA account rules. LawPay protects your IOLTA account against third-party debiting and commingling funds—ensuring compliance with ABA and IOLTA account rules.

Take our continuing legal education (CLE) course on law firm trust accounting to learn about the most common misunderstandings, what belongs in the account, and other best practices to remain compliant.

Choose an Accounting Method

You'll also want to decide how your firm will track incoming and outgoing funds. Your business's accounting method will affect cash flow, tax filing, how you manage your law firm’s chart of accounts, and even how you do your bookkeeping. You'll need to choose an accounting method before your firm files its first tax return and then stick with it on all subsequent returns.

Law firms can elect to use one of two accounting methods: cash accounting or accrual accounting.

Cash accounting

Cash accounting recognizes revenues when cash is received, as well as expenses when paid. However, this method does not recognize accounts receivable or accounts payable. Most law firms use cash basis accounting because it's simple to maintain.

Pros:

Easy to determine when a transaction has occurred

Straightforward to track how much cash the business actually has at any given time

Income isn't taxed until it is in the bank

Cons:

A limited look at your income and expenses

More IRS guidelines and restrictions

Accrual accounting

Accrual accounting records revenues and expenses when earned and incurred, regardless of when the money is received or paid. For example, when you send an invoice to a client, you'll mark it as revenue, even though you might not get paid for 30 days.

Pros:

More realistic idea of income and expenses during a period of time

Better for firms that experience large, rapid changes in their revenues

Cons:

Doesn't clearly indicate a business's actual cash flow

Must offset risks by carefully monitoring cash flow with accounts receivable and accounts payable

Set Up Multiple Payment Methods

Providing multiple alternative payment methods can make it easier for clients to handle their bills without visiting your office or mailing a check. Flexibility can improve your law firm’s account receivable process and help you get paid faster.

Our 2024 Legal Industry Report revealed that those who offered online payments had a 50% invoice recovery rate compared to those who offered checks and cash.

Payment options can include:

Credit and debit card payments

Tap to pay transactions with physical or virtual cards

Using LawPay as your legal payment processor makes it easy to securely offer multiple payment options while maintaining trust account compliance.

LawPay helps prevent commingling by keeping earned and unearned funds separate, preventing third parties from debiting your trust account, and only debiting your operating account for processing fees.

Automatically maintaining IOLTA-account compliance with LawPay and centralizing case and financial data in MyCase helps save your firm from the time and labor needed to manually track transactions. When your data is in one place, you can quickly complete three-way trust account reconciliation without toggling between different platforms and spreadsheets.

Keep Comprehensive Records

Your bookkeeper, CPA, and the IRS all require you to keep documents proving your income, credits, and attorney tax deductions.

Therefore, you should hold onto the following:

Receipts

Bank and credit card statements

Bills

Canceled checks

Invoices

Proof of payments

Financial statements from Bench or your bookkeeper

Previous tax returns

W2 and 1099 forms

Accounts receivable journal showing billed receivables

Case time records per client

Time summary reports sorted by attorney and by client

Register of cases in progress (often organized by client's name)

Other documents of income, deductions, or credits shown on your tax return

Keep these records for a specific time—some require 10 years, and some as few as three. The IRS doesn't require you to keep records of certain expenses under $75, but we still recommend, to be safe, you keep copies of all records.

Becoming a paperless law office can help your law firm operate more efficiently by ensuring documents are securely stored in one place. You can quickly find what you need at the click of a button rather than spending time searching file cabinets.

LawPay houses all of your payment data on one platform so you can quickly see the status of your clients’ accounts. You can also automatically generate, store, and send invoices all on the platform.

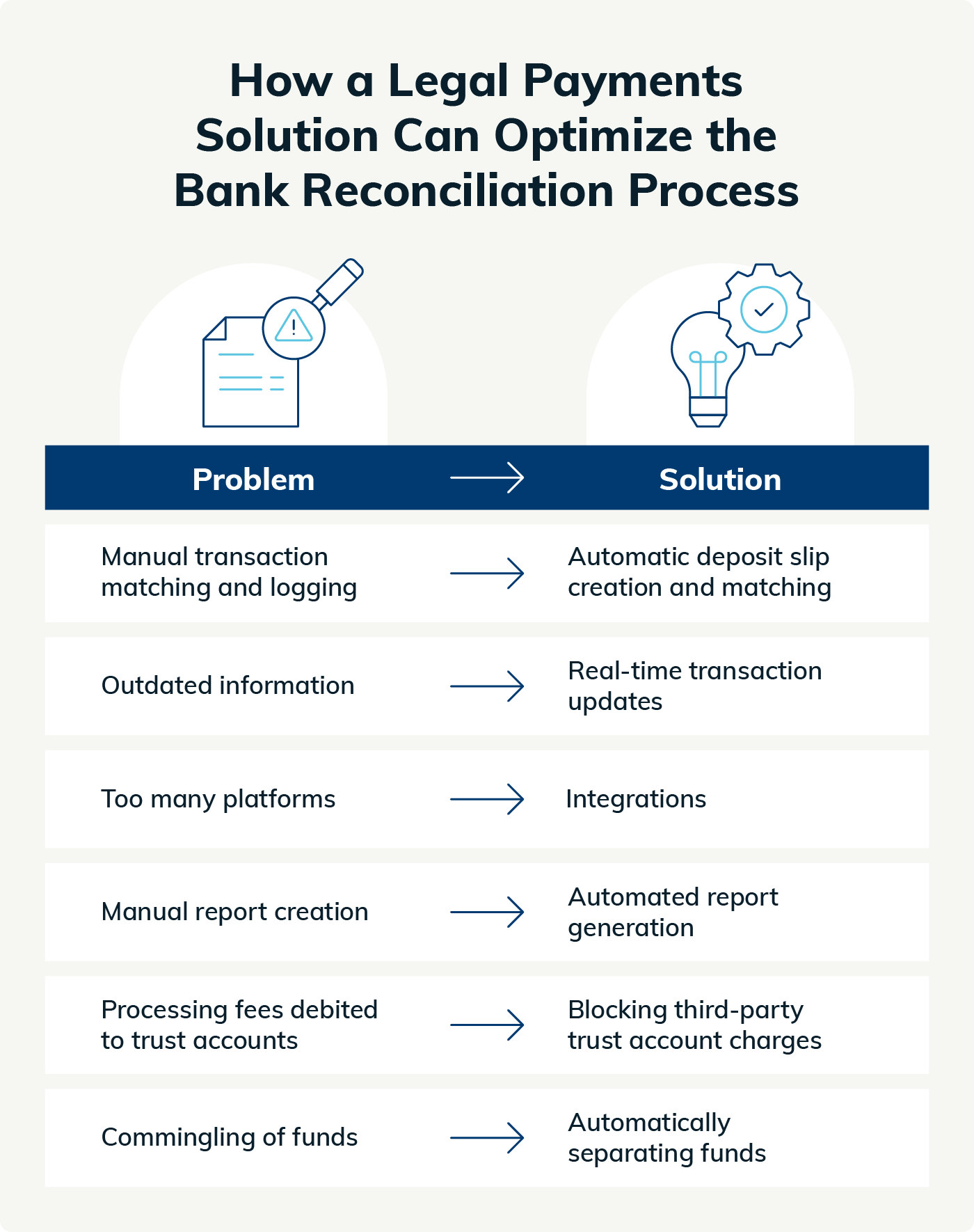

Regularly Reconcile Accounts

Law firms must ensure bank statements, trust account ledgers, and client ledgers match and are accurate. This is done by completing three-way trust reconciliation between all of these statements.

To do this, you’ll first compare the bank statement with the trust account ledger to ensure all entries match. If they don’t match, you’ll need to make corrections until they do. Then, compare the bank statement with each client ledger to ensure they also match. You must regularly reconcile accounts to comply with IOLTA requirements and maintain an accurate picture of your law firm’s finances.

However, the process can become tedious if you haven’t kept up with transactions throughout the month and don’t have statements handy.

With MyCase Accounting, you can automate the majority of the bank reconciliation process. Connecting your bank account will automatically sync all transactions to our platform. When you enable Automated Smart Deposit and use MyCase with LawPay, our solution will generate deposit slips and match them to transactions. This ensures less time spent and fewer errors from manually matching transactions.

Download our eBook, "A Guide to Ensuring IOLTA Account Compliance" to learn how trust accounts work, how to properly set up an IOLTA account, and how LawPay can help simplify the trust accounting process.

Frequent Law Firm Accounting Issues

Law firm accounting is a challenging function for all law firms. Lawyers must keep track of a surplus of information across multiple sources. We’ll go over a few of the most common issues and solutions.

Experiencing Cash Flow Challenges

Poor accounting processes can result in an unhealthy cash flow. Late payments, delayed invoicing, and excess overdue payments make it challenging to financially operate. Many of these issues can stem from manual or tedious methods that fuel hours of non-billable work.

Solution: Adopt several payment methods, use a legal billing platform like LawPay to instantly generate and send electronic invoices, and schedule automatic payment reminders and follow-ups to optimize your law firm’s cash flow.

Violating Trust Accounting Requirements

Trust accounting rules requires law firms to closely manage each of their client’s trust funds to avoid misappropriation. As easy as it may sound, it can quickly become a major hurdle for those who are manually tracking funds. For example, accidentally depositing trust funds into your operations account is a major violation.

Managing funds is only half the battle. Maintaining accurate ledgers and routinely reconciling accounts can also take up a lot of time. For example, you must maintain an accurate ledger for each client in case they ask for their account’s status. If you’ve had several unlogged transactions throughout the week, you would need to spend time finding deposit slips, double-checking spreadsheets, and manually calculating balances to get that information to clients in a timely manner.

Solution: Use a legal accounting solution like MyCase to automatically sync information, manage client trust fund balances, and perform bank reconciliation with ease.

Struggling To Manage Client Payments, Billing, and Collections Data

Failing to consistently and accurately record transactions can lead to difficulties managing cash flow, performing three-way trust reconciliation, and understanding your law firm’s financial health in real time.

Solution: Use a legal payments processor like LawPay to house your payment processing information on one platform.

Why Is Accurate Law Firm Accounting Important?

The success of your law firm depends on effective accounting. The firm needs a clear, accurate accounting system to get a complete financial picture and meet its obligations to clients, the state bar, and the firm. Here's why:

You need to stay compliant. Compliance regulations can vary depending on where you practice law, but violating legal accounting rules could lead to significant financial penalties, license suspension, or even disbarment.

You need to grow your business. With law firm accounting, you can collect, analyze, and make data-driven decisions based on the money coming in and going out of your firm. Using this information, you can also identify which parts of your practice are the most and least successful so that you can allocate resources more thoughtfully in the future.

You need to manage your reputation. A lawyer's reputation is crucial. Accounting mistakes make you look unprofessional. And a lack of professionalism can lead to losing your clients, referrals, and growth opportunities.

Optimize Your Law Firm’s Accounting System With MyCase and LawPay

Accounting for lawyers may be new or challenging to you, but it doesn't have to be scary. What's most important is that you get the details right to stay compliant with ethics rules and help your firm grow to its full potential.

From sending payment requests and tracking them to integrating with your go-to legal software products, LawPay’s legal billing software will fit your needs. LawPay also ensures your law firm accepts payments that comply with your state bar's regulations surrounding trust (IOLTA) accounts and the American Bar Association (ABA) guidelines.

Additionally, pairing LawPay with MyCase Accounting can help your law firm ensure that your payments are compliant, accurately logged, and housed in one place to easily reconcile accounts and get a complete view of your law firm’s finances.

To learn more about how MyCase and LawPay can help your firm and how you can avoid legal accounting mistakes, schedule a demo today.

About the author

Hannah DeFreitas (née Bruno) is a Senior Content Strategist and Blog Specialist for 8am, a leading professional business solution, and a senior content writer for 8am. Her work spans long-form articles, thought leadership, product storytelling, and conversion copy that distills complex legal and fintech topics into clear, human language. With nearly a decade of experience, she specializes in transforming research and data into narratives that enable professionals to work smarter and serve their clients more effectively.